Your Emergency Fund Isn’t Failing Because You’re Undisciplined

You’ve got ₱15,000 in your “emergency fund” account. Then your nephew’s graduation comes up, and you need ₱3,500 for the gift. It’s not really an emergency, but it’s important, and the money’s just sitting there. Two weeks later, your barkada plans a beach trip—₱6,000. You tell yourself you’ll pay it back. By the time an actual emergency hits—your phone screen cracks, or you need to rush home to the province—the fund is at ₱2,500, and you’re borrowing from next month’s budget again.

Here’s what most financial advice gets wrong: it assumes the problem is discipline. That if you just tried harder, resisted more, cared more about your future self, you’d stop touching that money. But the real issue isn’t willpower. It’s that we’re asking one account to do too many jobs.

Why Your Emergency Fund Keeps Getting Raided

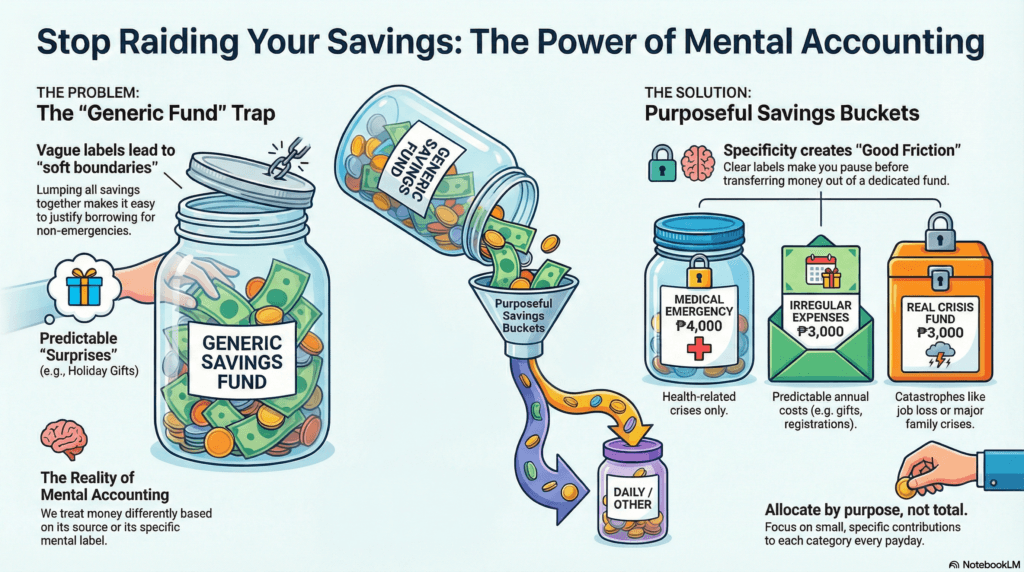

In The Psychology of Money, Morgan Housel writes about how people don’t actually treat money as interchangeable, even though logically it is. A thousand pesos is a thousand pesos—but our brains don’t work that way. We treat “birthday money from Lola” differently from “overtime pay.” We treat “savings” differently from “investment.” This isn’t irrationality. It’s something behavioral economists call mental accounting—our tendency to assign different values and rules to money based on where it came from or what we’ve mentally labeled it for. And when you lump everything—actual emergencies, future goals, upcoming expenses you know are coming—into one generic “emergency fund,” you’re setting yourself up to raid it. Because the label is too vague. The boundaries are too soft.

It’s Time to Split Your Savings

The solution isn’t to save more. It’s to save separately. Not one emergency fund—three or four distinct envelopes, physical or digital, each with a single, non-negotiable job. One account is for medical emergencies only. One is for “expected irregulars”—the birthday gifts, the annual car registration, the holiday expenses you know happen every year but still somehow surprise you. One is for bigger goals, like moving out or starting a small business. One is for pure catastrophe—job loss, family crisis, the things we don’t want to name but need to prepare for.

This isn’t just semantics. When money has a clear, specific purpose, your brain treats it differently. It stops being “extra money I can borrow from.” It becomes “the thing standing between me and financial catastrophe if I lose my job” or “my cousin’s tuition fund that I promised to help with.” The specificity creates friction—the good kind, the kind that makes you pause before transferring it out.

Separate Accounts for Predictable “Surprises”

Here’s the part that matters for us: Filipino financial life is full of irregular but predictable expenses that we keep treating as surprises. Pasko. Fiestas. Tuition. Someone’s hospital bill. These aren’t emergencies—they’re recurring costs we’ve been trained to absorb as “part of life” without planning for them. So we pull from savings, feel guilty, restart from zero, repeat. That cycle doesn’t break with more discipline. It breaks with better categories.

Tonight, look at your bank app. If you’ve got one lump sum sitting there labeled “savings” or “emergency,” split it. Even if it’s just ₱10,000 total. Put ₱4,000 in “Medical Emergency—Do Not Touch.” Put ₱3,000 in “Irregular Expenses I Know Are Coming.” Put ₱3,000 in “Real Crisis Fund.” The amounts don’t matter yet—the separation does. Then, moving forward, every time you get paid, allocate by purpose, not by total. ₱500 here, ₱1,000 there. Small, specific, protected.

The goal isn’t perfection. It’s clarity. When your money knows its job, you stop asking it to do everything—and it finally starts doing something.

A BantayDailyPH Daily Dose editorial.